For over a decade, fraud prevention has focused on perfecting the selfie: sharper liveness detection, more accurate facial matching, better document forensics. The assumption was simple: if you can verify that what someone submits is real, you can trust them.

That assumption is no longer valid.

Smile ID’s analysis of over 200 million anonymised identity checks conducted across East, West, Central, and Southern Africa in 2025, spanning 37 industries in over 35 countries, reveals a fundamental shift:

Fraud defence is no longer in the validity of a selfie. It's in everything the selfie can't tell you.

What Selfies Can't See

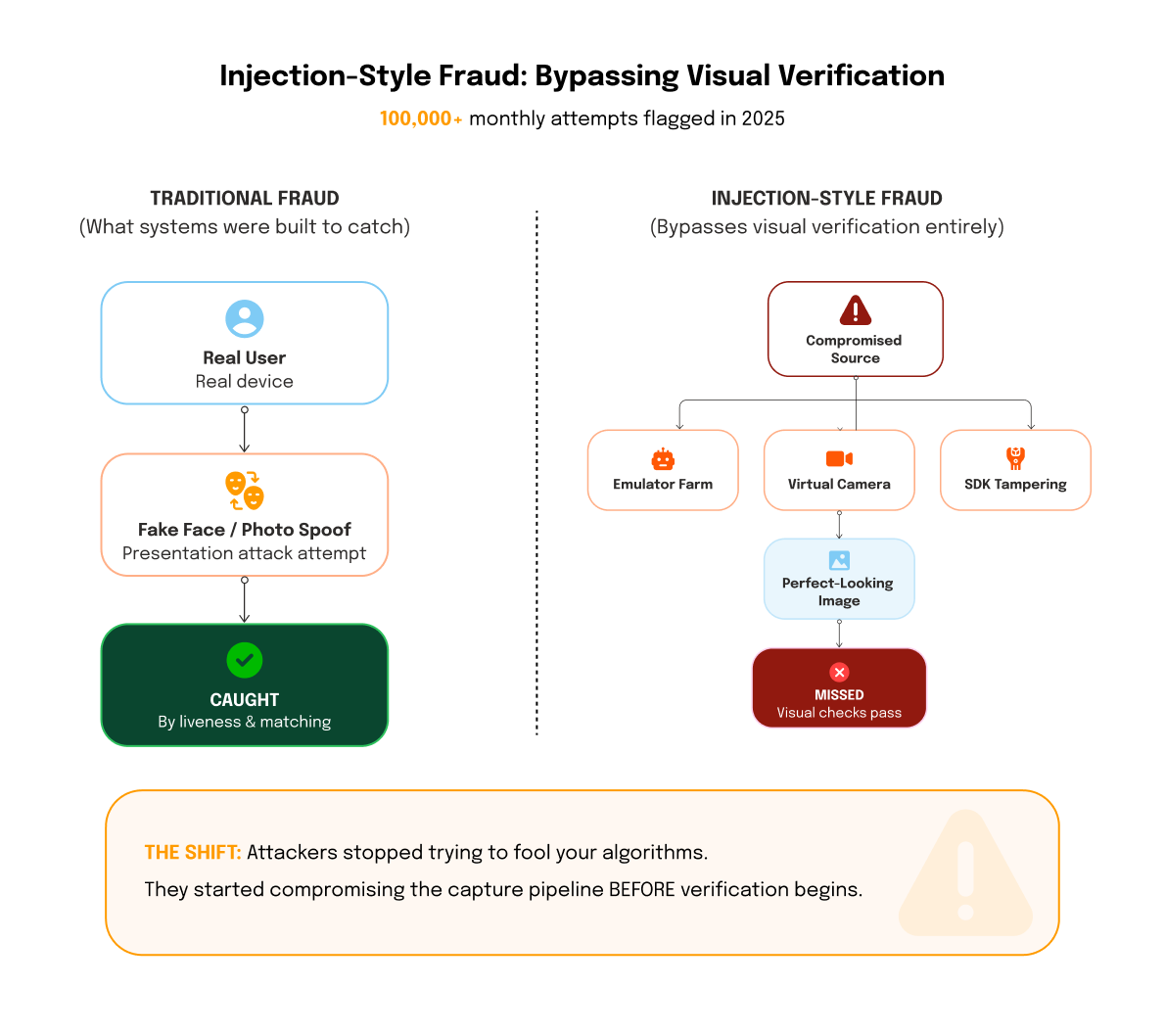

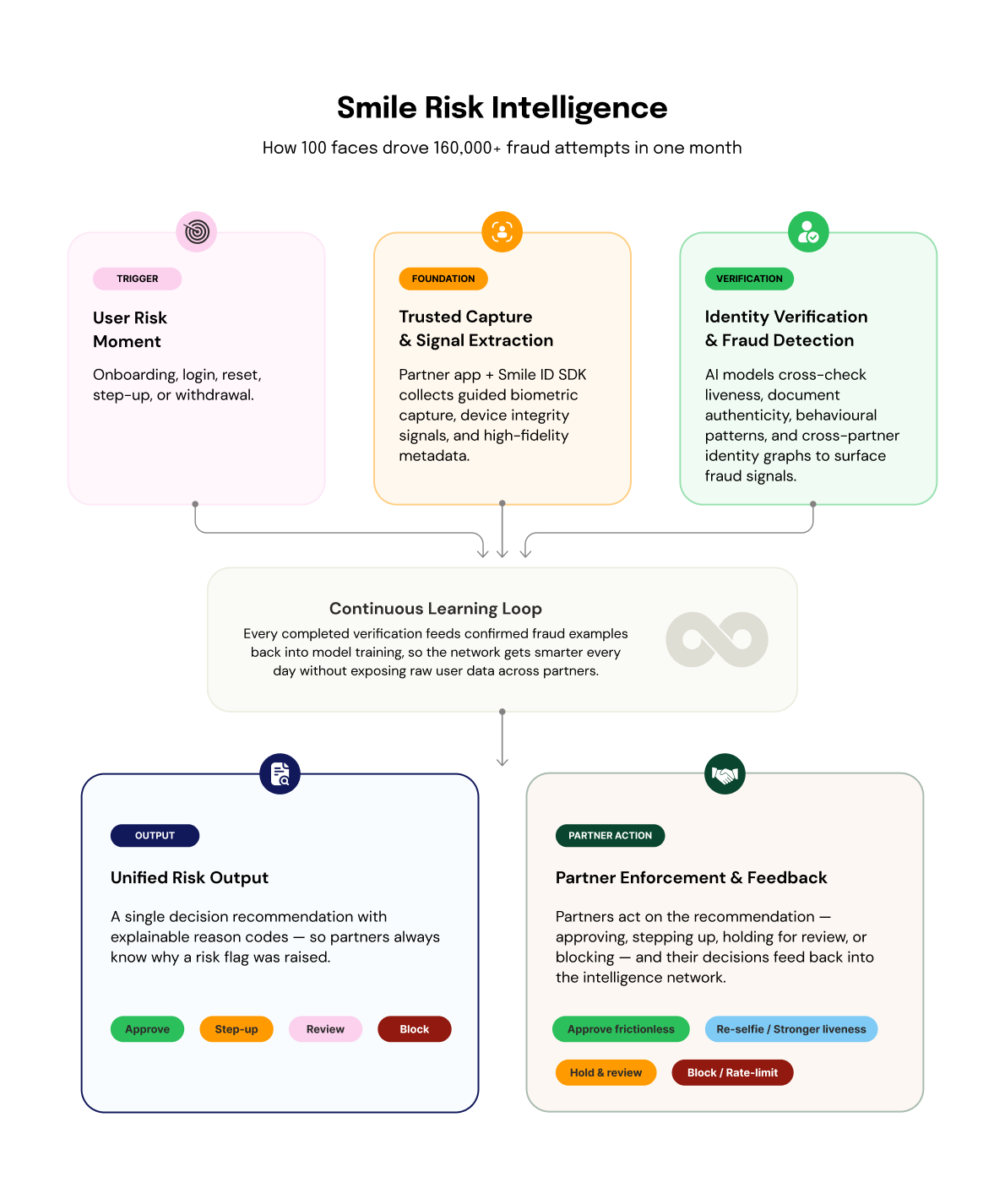

In 2025, Smile ID detection systems flagged over 100,000 injection-style fraud attempts per month, cases where attackers didn't try to beat facial recognition or fool liveness checks. They attempted to bypass the visual layer entirely by compromising how images were captured and delivered.

Emulator farms running hundreds of parallel attempts. Virtual cameras feed pre-recorded or AI-generated media directly into verification flows. APP tampering that forges device signals to mimic legitimate hardware.

These attempts look visually perfect: clean selfies, matching documents, no obvious spoofing. The fraud isn't in what you see. It's in what you can't see: how that image was created.

When the camera feed can be replaced, when device environments can be spoofed, and when capture integrity cannot be proven, visual analysis becomes structurally insufficient. A selfie is just data. If you don't know where that data came from, you can't trust it.

The biggest shift we see in 2026 is that fraud no longer looks like fraud at the point of verification,” said Mark Straub, CEO of Smile ID. “Most modern attacks pass individual checks and only reveal themselves when activity is connected across time and platforms. Treating identity as something you verify once is no longer defensible. Trust now has to be monitored, not assumed.”

3 Structural Shifts That Break Traditional Fraud Defence

Let’s examine the key structural shifts businesses must understand in today’s evolving fraud defence landscape:

1. Attackers Abandoned Onboarding for High-Value Account Access

Authentication-related fraud attempts now occur at 5× the rate of onboarding fraud.

Attackers have largely stopped creating fake accounts. The accounts being targeted already passed KYC. The fraud happens inside trusted systems: at login flows, password resets, device changes, and high-value withdrawals, where controls are designed for convenience rather than security.

In West Africa, retail banking fraud attempts rose approximately 50% year-over-year in 2025, driven primarily by authentication and account recovery flows. These touchpoints rely on lighter controls than onboarding: SMS OTPs that can be intercepted through SIM swaps, email links vulnerable to social engineering, and security questions that insiders can bypass.

The hardest problem is no longer proving who someone is at sign-up. It's keeping attackers out of already-verified accounts.

Most platforms still treat identity as a one-time checkpoint. Verify at onboarding, then trust indefinitely. KYC becomes a compliance checkbox, not a continuous security layer. But when fraud concentrates post-approval, that model fails structurally.

Fraud defence must operate continuously across the customer lifecycle at every high-risk moment where identity determines access. Instead of asking "Did this person pass KYC six months ago?", systems must ask: "Is this the same person who passed KYC, presenting from a trusted device, in a pattern consistent with their normal behaviour, at a time that makes sense?"

2. Fraud Became Repeatable, Automated, and Cross-Platform

Modern attackers operate as syndicates that reuse identity assets at scale, rotate through platforms systematically, and move faster than any single institution can respond.

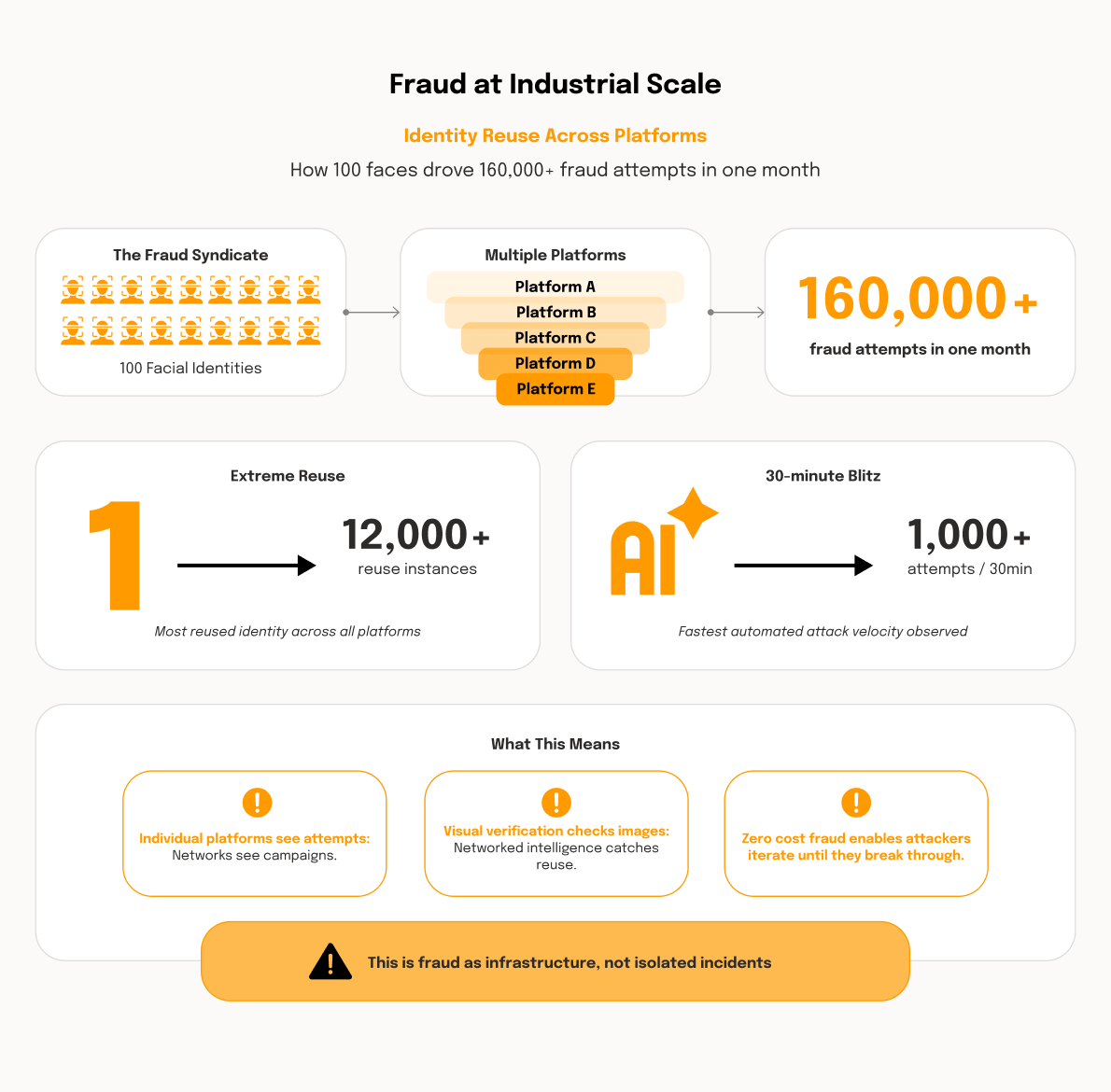

In one month, more than 160,000 fraudulent verification attempts were traced back to just 100 facial identities. Some of those faces appeared more than 12,000 times across multiple platforms. In another case, a single synthetic identity was re-attempted over 1,000 times within 30 minutes.

This is identity farming: attackers build supply chains of verified accounts, "age" them through dormancy or low-risk activity, then activate them in coordinated bursts for fraud or money laundering. By the time these accounts are weaponised, they look legitimate, trusted, and low-risk.

Smile ID's biometric deduplication solution, Smile Secure, detected 71% more duplicate fraud attempts in 2025 than the combined total of 2023 and 2024. These patterns are invisible to platforms operating in isolation.

Here's the structural problem: individual financial institutions see their own traffic. A verification attempt arrives. The selfie matches. The document looks clean. The device seems normal. The system approves.

What they don't see:

- That same face was used 200 times last week across 15 other platforms.

- That device identifier has been linked to 50 confirmed fraud cases elsewhere.

- The capture metadata is identical to patterns flagged in coordinated attacks across the network.

- This is the 47th attempt from this cluster in the past hour.

Signals only work when they're connected. A device fingerprint is just metadata. A face embedding is just a vector. A timestamp is just a number. But when you connect those signals across millions of verification attempts, across dozens of platforms, over time, patterns emerge. Reuse becomes visible. Coordination becomes detectable. Fraud infrastructure reveals itself.

Smile ID's Risk Intelligenceconnects signals across platforms, processing hundreds of millions of checks. When an injection technique surfaces in Kenya, that pattern strengthens defences in Nigeria within hours, not weeks. When a device cluster is linked to confirmed fraud in Ghana, that intelligence blocks similar attempts across the network before losses occur.

This is what makes networked intelligence different from isolated verification. A single platform sees attempts. A network sees campaigns. A single platform detects anomalies. A network detects coordination. When attackers already operate as syndicates, network defence must operate as infrastructure too.

3. Fraud Moved from Visual Deception to Pipeline Compromise

The shift from selfies to signals isn't just about attacker sophistication. It's about economics.

Generative AI has fundamentally altered the cost structure of attempting fraud. High-quality synthetic documents, deepfake imagery, and automated biometric manipulation are no longer expensive or rare. What once required specialist skills and significant resources can now be produced cheaply, repeatedly, and at scale.

When the marginal cost of fraud attempts approaches zero, attackers don't need to succeed on the first try. They iterate continuously until systems break. Any control that assumes scarcity of attempts, identities, or attacker capability will be systematically overwhelmed.

As fraud becomes automated and repeatable, the capture environment becomes as important as the biometric itself. Attackers exploit the weakest link: not the verification algorithm, but the systems that produce the input.

Attackers Now Target the Pipeline, Not the Algorithm

This economic shift changes where attackers focus their efforts. When creating synthetic media costs nothing, the bottleneck isn't making convincing images; it's getting them into verification systems undetected.

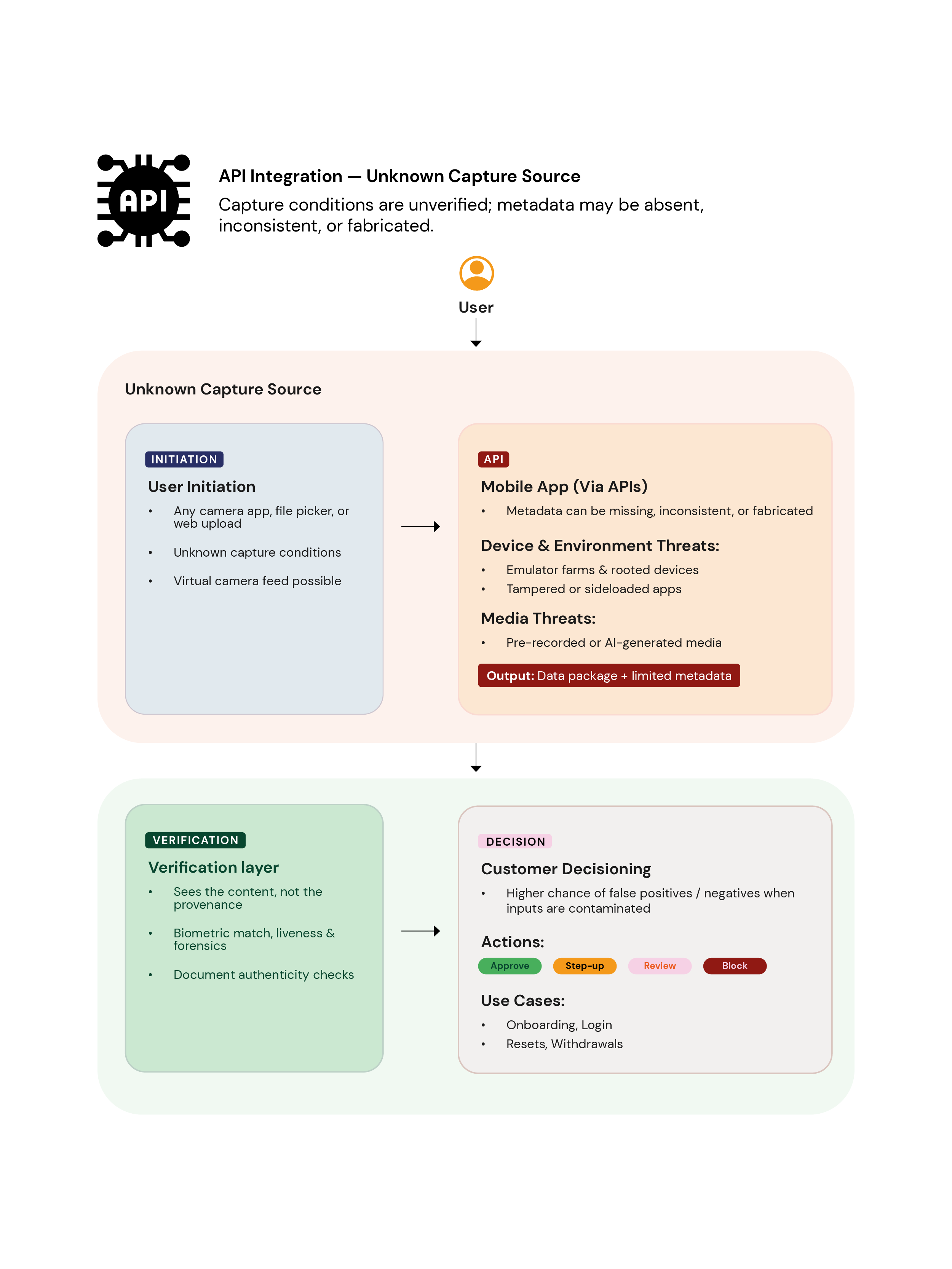

API-based verification flows see only the final output: a selfie, a document with limited visibility into how that media was produced. If the camera feed has been replaced with a virtual camera, if the app environment has been tampered with, or if the device is an emulator running automated scripts, the verification data is compromised before any analysis begins.

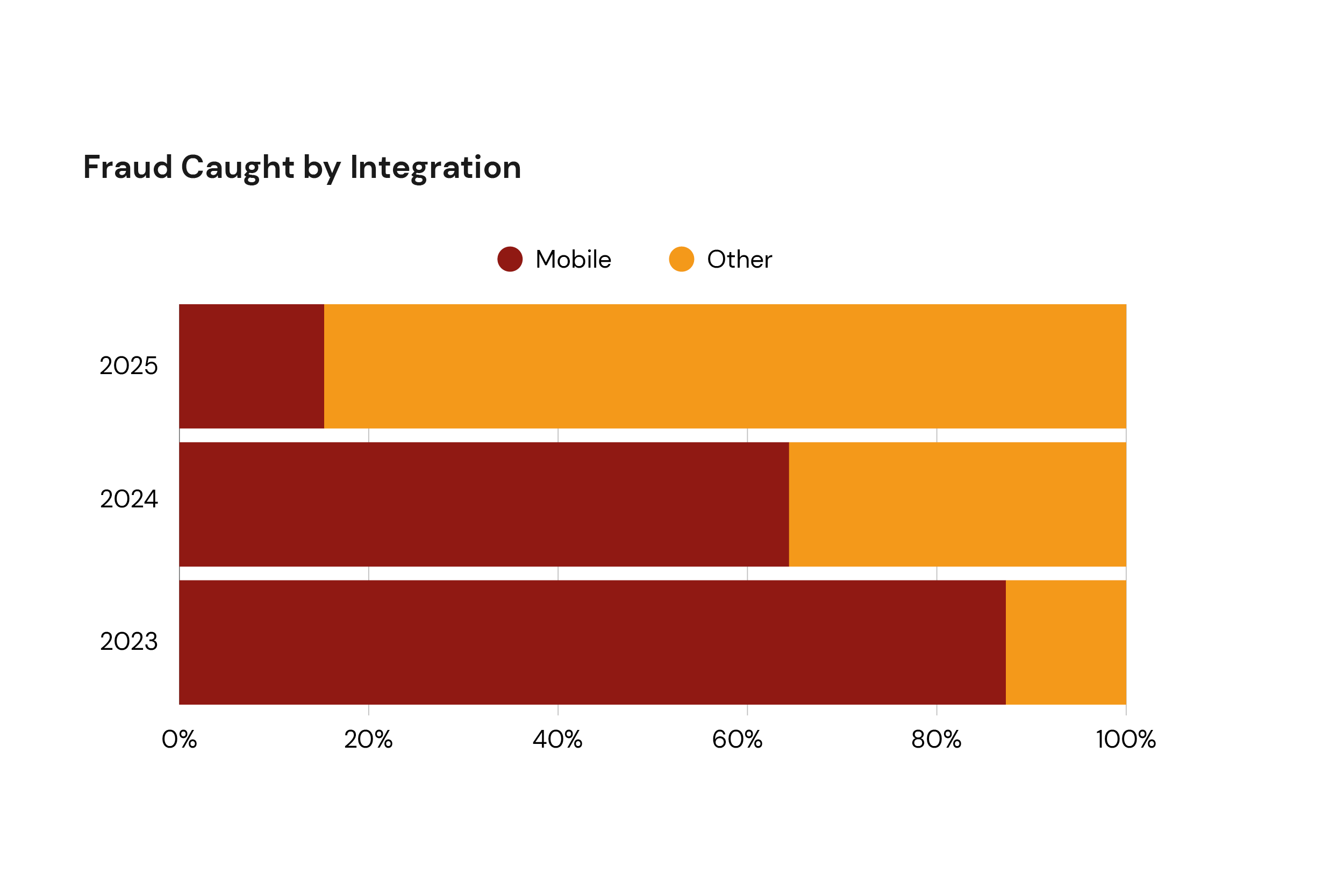

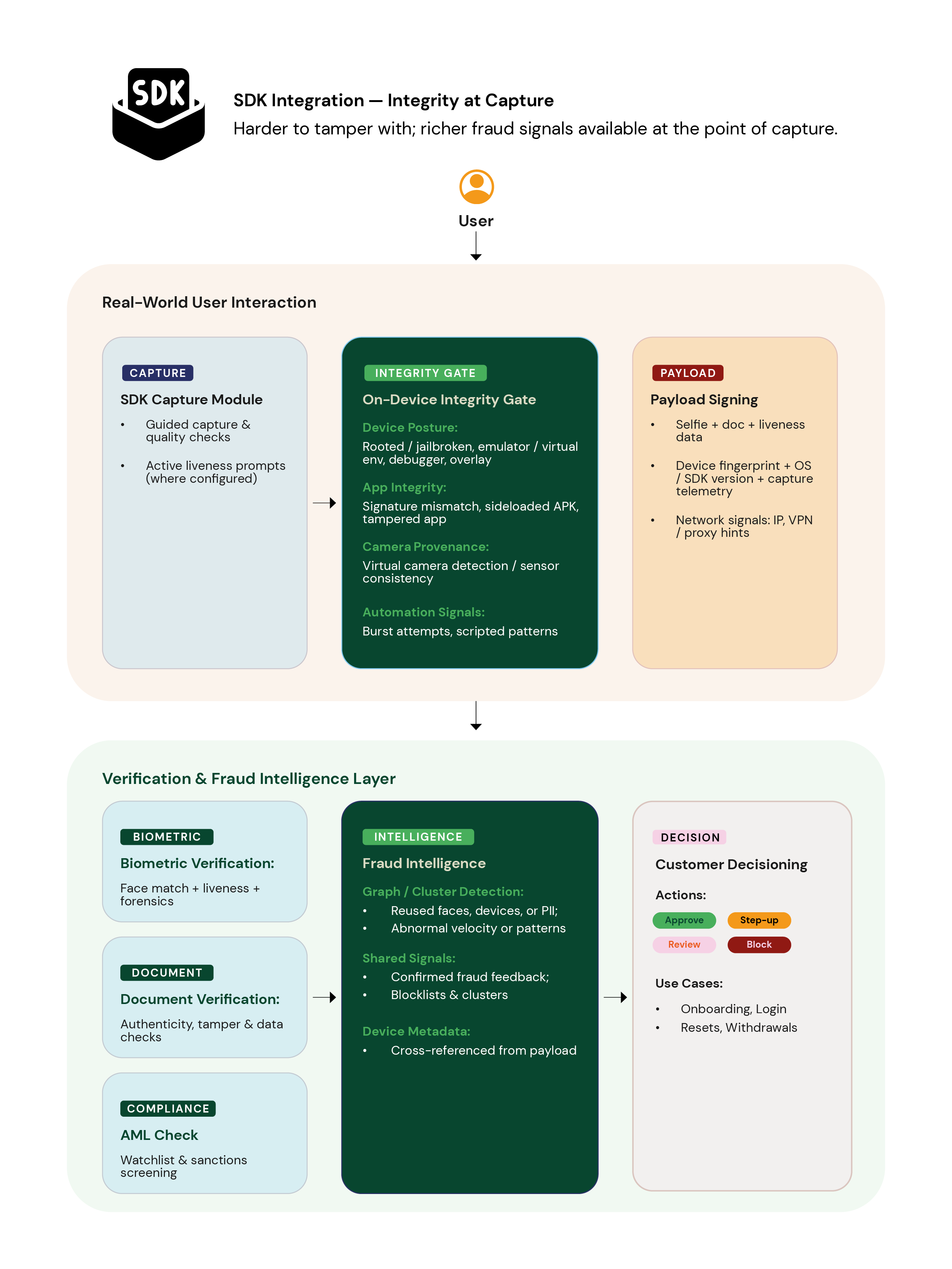

Mobile SDKs close this gap by validating capture at the source. They collect on-device signals, assess environmental integrity, and analyse behaviour, proving not just what was submitted, but how it was created. This is why SDK-based flows accounted for nearly 90% of fraud rejections in 2025, up from 15% in 2023: they expose pipeline compromise that API-only verification cannot see.

Signals reveal fraud that selfies cannot.

The full report includes detailed regional breakdowns with fraud technique classifications, attack pattern analysis, and infrastructure-specific defence recommendations.

Networked Fraud Intelligence: How Financial Institutions Must Adapt in 2026

The three structural shifts above: fraud moving to high-value post-approval moments, operating as repeatable cross-platform campaigns, and compromising capture pipelines, converge on a single operational reality: effective fraud defence requires connecting signals that reveal patterns invisible to isolated transaction checks.

Modern fraud operates through systematic identity reuse. Attackers don't attempt once and move on; they retry the same assets repeatedly, testing until they find a gap. What looks like separate legitimate attempts may be the same face trying to open multiple accounts on your platform, or the same device cluster rotating through different credentials in coordinated bursts.

This creates detection gaps. Without connecting signals across attempts, sessions, and platforms, you cannot see that the same face is trying to create five accounts on your platform this week, that a single device is being used for 50 onboarding attempts with different identities, that an identity approved on your system has been reused 200 times across the ecosystem, or that capture metadata matches attack patterns detected elsewhere in the network.

Fraud syndicates exploit this blindness: they probe platforms repeatedly until they succeed, rotate the same identity assets across multiple institutions, and move faster than isolated defences can respond.

Smile ID's approach to fraud prevention is built on this networked intelligence model:

Smile ID's Risk Intelligence is built on networked intelligence. Our SDK integrations capture comprehensive fraud signals beyond biometric images: device integrity, capture environment, behavioural context, and metadata consistency, which is why SDK-based verification accounted for nearly 90% of fraud rejections in 2025.

Our biometric deduplication solution, Smile Secure, prevents the same individual from creating multiple accounts on your platform and detects identity reuse across our network of hundreds of millions of checks.

3 Strategic Priorities for Fraud Defence in 2026

These three shifts: lifecycle-based attacks, networked fraud infrastructure, and pipeline compromise, require a new defensive model. Three priorities must anchor fraud strategy in 2026:

Priority 1: Build Networked Fraud Intelligence Across the Full Lifecycle

Move beyond one-time KYC to continuous risk assessment. Connect signals across time, sessions, and platforms to expose coordination that single checkpoints miss. Identity assurance cannot end at account creation; it must extend to every moment where identity determines access. E.g login, recovery, device changes, withdrawals. etc.

Key Action:

- Monitor behavioural signals for fraud across the customer lifecycle.

- Layer biometric re-authentication with device validation and behavioural consistency checks.

- Consistently analyse gathered signals and patterns to stay ahead of fraud

- Treat re-authentication with the same rigour as onboarding.

Priority 2: Harden Authentication at High-Value Moments

With authentication fraud at 5× the rate of onboarding, proportionate controls must protect the moments that unlock value. Password resets, device authorisation changes, and withdrawal approvals. These flows are often designed for convenience, and the structural weakness is what attackers exploit.

Key Action:

- Apply biometric authentication at high-risk points, not just onboarding.

- Validate the individual's integrity before approving sensitive changes.

- Flag abnormal behaviour patterns: dormant accounts suddenly active, rapid transaction sequences, geographic anomalies, and require additional verification.

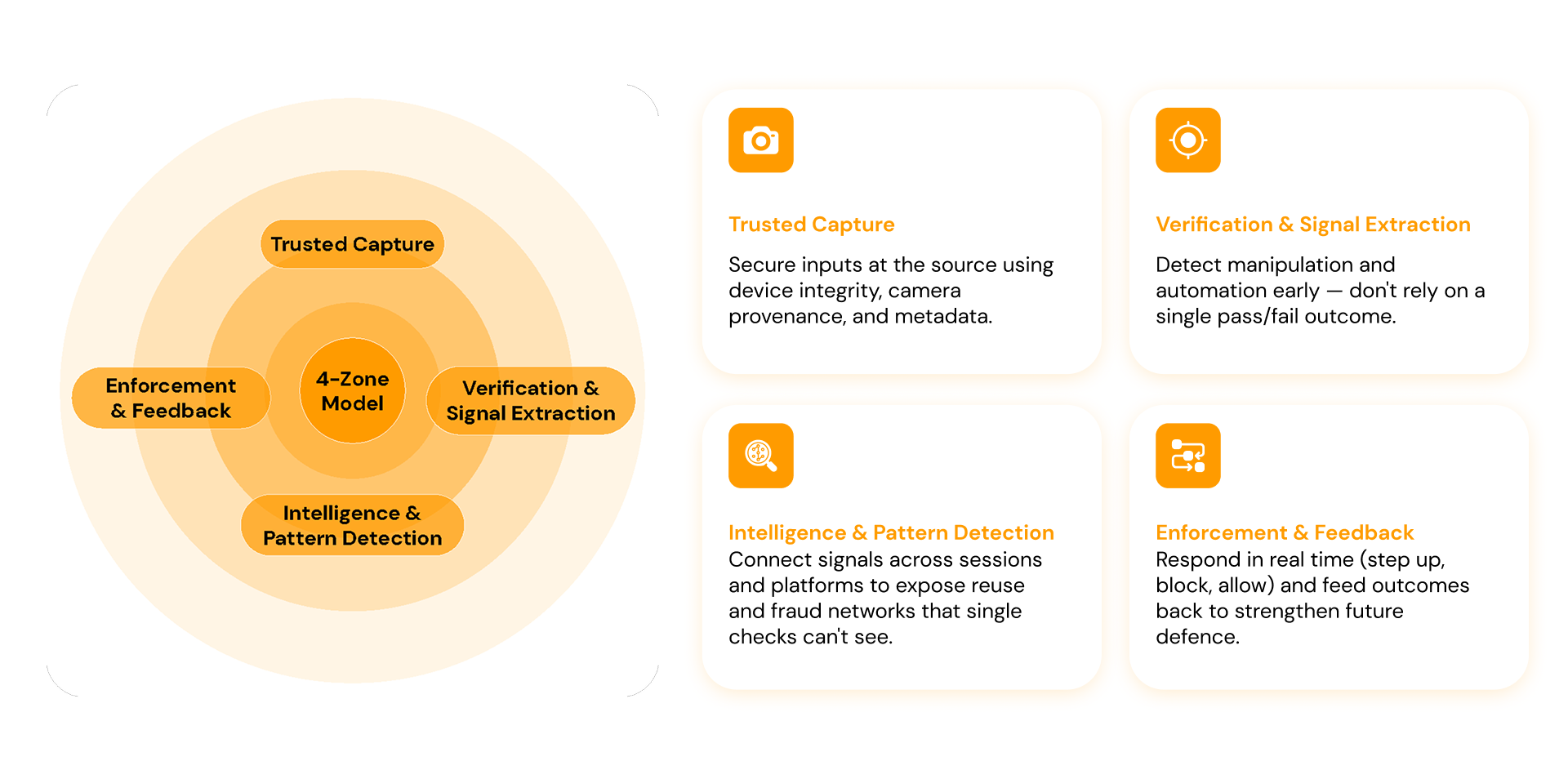

Priority 3: Protect Capture & Device Integrity at Source

Validate how evidence is created, not just what it contains. Implement SDK-enforced capture that proves media came from a real device in a trusted environment. Layer device-level validation, environmental checks, and metadata consistency to detect pipeline compromise before images reach verification.

Key Action:

- Prioritise SDK integrations over API-only flows where security matters most.

- Capture device fraud signals, including behavioural telemetry and environmental context.

- Connect those signals to network intelligence so injection attempts, emulator farms, and coordinated campaigns become visible and blockable in real time.

API integration leaves penetration gaps

More Secure SDK Integration

The 4-Zone Defence System for Modern Fraud Prevention

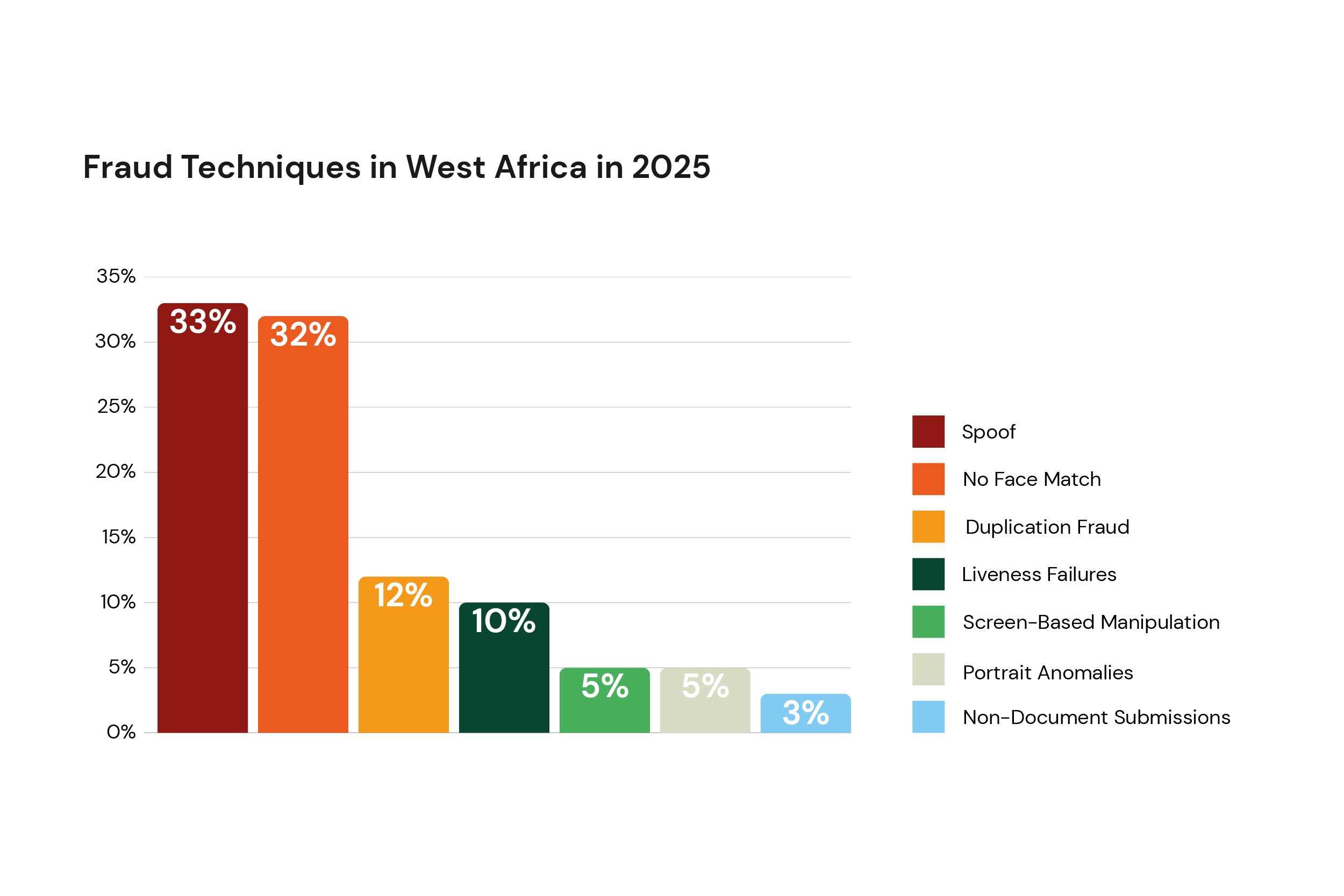

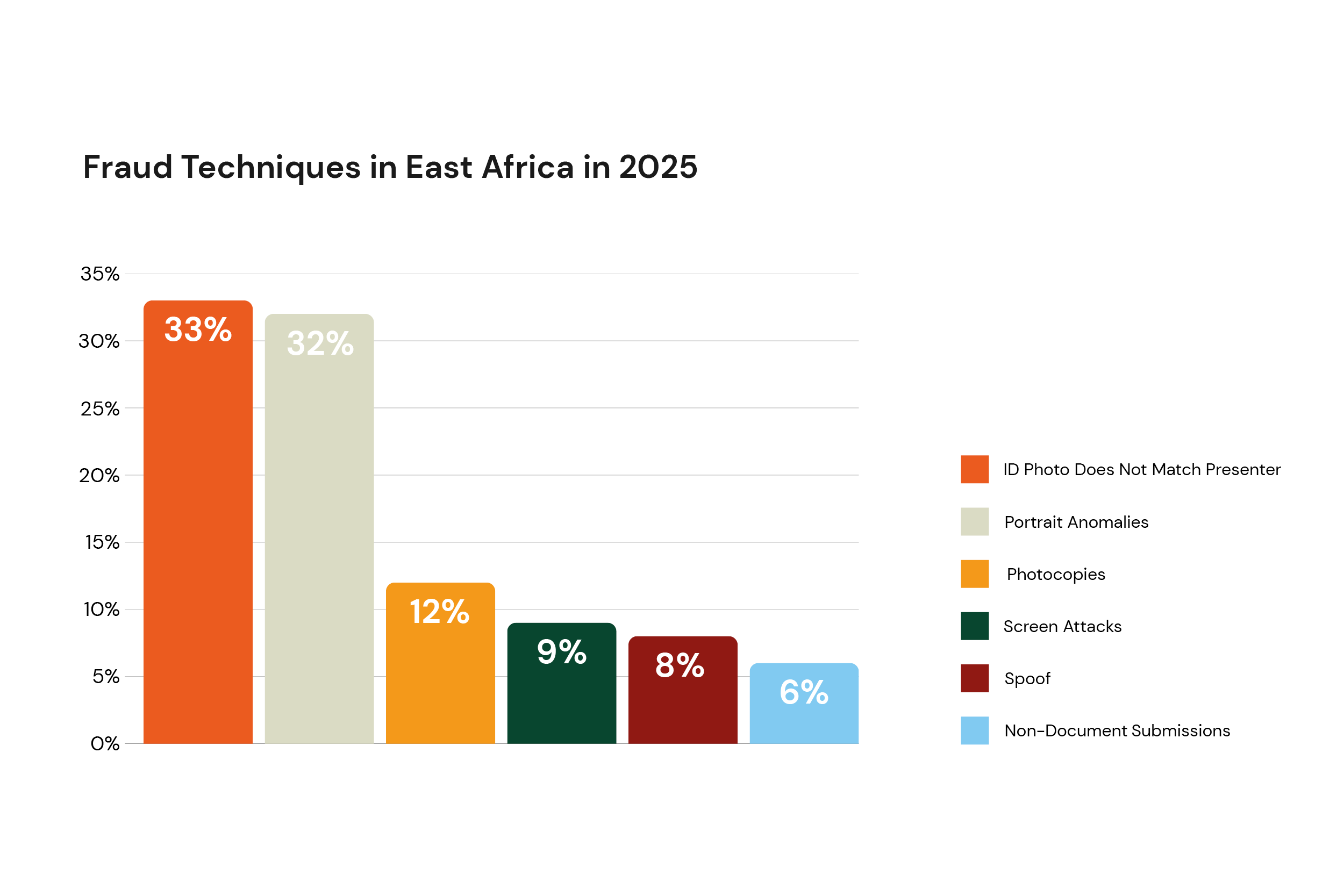

How Fraud Plays Out Across Africa

While the shift from selfies to signals is universal, how fraud manifests varies by region based on infrastructure maturity and regulatory context:

- West Africa: Identity farming and insider-assisted account takeovers dominate. Attackers source real credentials, use agent-assisted flows to get accounts approved, then weaponise those "trusted" accounts later. Signals that detect identity reuse, device clustering, and abnormal post-approval behaviour become critical.

Impersonation makes up about two-thirds (65%) of potential fraud attempts in West Africa, driven by spoofing and no-face-match during biometric verification.

- East Africa: Document manipulation drives fraud in hybrid verification journeys where flows rely on user-submitted ID photos rather than real-time biometric checks against authoritative databases. About 60% of rejections stem from document integrity issues: portrait anomalies, photocopies, screen attacks. Signals around capture timing, device consistency, and portrait forensics are essential.

In East Africa, about 3 in 5 verifications rejected for potential fraud are due to document integrity issues.

- Southern Africa: AI-assisted biometric impersonation has become the dominant threat. Deepfake attempts surged from under 200 monthly in 2024 to over 3,000 by year-end 2025. Multiple central banks issued warnings about AI-generated videos impersonating officials to promote fraudulent schemes. Signals that detect synthetic media generation artefacts and behavioural inconsistencies separate real users from AI-generated attacks.

Fraud is overwhelmingly biometric in South Africa: nearly 9 in 10 verification attempts rejected for potential fraud are due to impersonation and spoofing (47% no-face-match and 40% spoofing) during biometric verification.

- Francophone & Central Africa: Regulatory constraints and connectivity gaps increase reliance on document-based flows where provenance cannot always be proven. Assisted capture and deferred uploads are common. Signals around submission timing, device reuse, and cross-platform patterns detect when "clean-looking" documents are being recycled across fraud campaigns.

About two-thirds of all rejected verifications were due to suspected document fraud, led by portrait anomalies (22%) and photocopies (20%), with no face match (26%).

In Central Africa, the single biggest potential fraud rejection reason is no face match during document verification (36%), about 1 in 3 flagged cases.

Regardless of region, the defensive imperative is the same: move from visual verification to signal intelligence, from one-time KYC to lifecycle monitoring, from isolated controls to networked defence.

Why This Matters Now

Africa's digital economy added approximately 200 million new financial accounts in the past decade. Financial inclusion in Sub-Saharan Africa rose from 34% to nearly 60%. But security infrastructure has not kept pace with that expansion.

Systems that only verify what users submit without validating how it was created, without connecting attempts across time and platforms, without extending verification beyond onboarding into the full lifecycle, are defending against yesterday's threat model.

The fraud infrastructure already exists, operating as networks, reusing identities at scale, targeting post-approval flows, compromising capture pipelines. Meanwhile, the industry is still optimising selfies. The attackers moved on months ago.

This report provides the operational blueprint for closing that gap before it becomes systemically destabilising. The full analysis includes fraud technique classifications, SDK vs. API detection performance data, identity farming patterns, regional attack vectors, and implementation guidance for financial institutions, fintechs, and digital platforms operating across Africa.

.png)